Market Economics

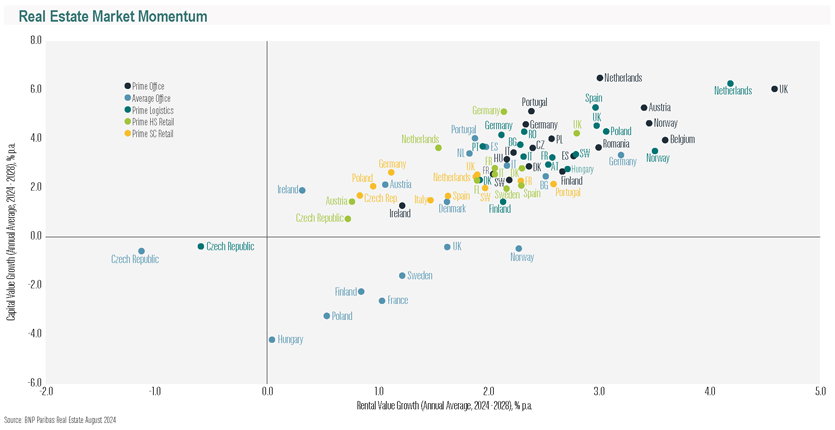

Real estate recovery expected across several markets

The overall outlook for the European real estate market is positive. By next year, residential property prices are expected to rise in most regions – particularly in major cities – with the notable exception of Germany. Rents are increasing at a rapid pace. The office sector is beginning to regain momentum, while retail is slowing – although luxury retail remains resilient. Meanwhile, the hotel industry is booming, and logistics continues to perform strongly. Forecasts for the remainder of 2024 are favourable, with easing inflation prompting cautious optimism among buyers. These trends were revealed in a recent analysis by Re/MAX Europe focusing on Italy, Germany, Austria, Spain and the Czech Republic. While Germany experienced a decline in house prices during the first half of 2024, including a 5.2% fall in Berlin, prices in Spain have been rising sharply, with more than 9% growth in Barcelona and Madrid. Vienna and Prague also saw price increases of 5.3% and 7%, respectively, over the same period. House prices in Italy have remained stable throughout 2024, but are expected to grow in 2025.

At the same time, rents are rising across Europe, driven by inflation and the growing difficulties in obtaining mortgages. The increases range from 9.6% in Berlin to an average of 7.6% in Italy (driven by the short-term rental market) and 5.3% in Vienna, with more moderate increases in the Czech Republic. BNP Paribas expects the European real estate market to continue its recovery through to the end of 2024.

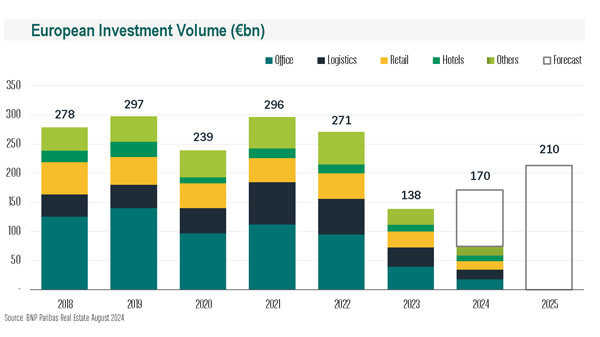

“Sentiment has generally seen a marked positive shift with increases in activity in most of Europe,” states the BNP Paribas European Property Market Outlook Report for the second half of 2024. Italy recorded the largest growth during the first half of the year, with transaction volumes reaching €3.2 billion (+55% compared to the same period last year), albeit from a low base. The UK recorded €27 billion (+8%), Germany €12.2 billion (+34%) and Spain €4 billion (+3%). The only major market to see a fall in activity was France, at €5.9 billion (-29%).

According to the French bank’s report, the residential sector remains the primary focus for investors, followed by the industrial and logistics sectors. Despite some uncertainties, the office market continues to be liquid and attractive. Competition among investors and the influx of capital into commercial real estate are expected to influence pricing and yields, “with gradual appreciation anticipated for residential and logistics properties, alongside increased capital allocation to alternative and niche assets”. According to the Outlook of Scenari immobiliari, Italy is projected to lead the EU market in terms of growth during 2024-2025, with real estate turnover expected to increase by 3.4% by the end of 2024 and by 5.7% in 2025. The number of residential transactions is projected to reach 700,000 in 2024 and around 760,000 in 2025, with stronger demand for new or higher quality homes that do not require renovation. House prices will also rise (with an average expected increase of 3.1%), although the increases will be most significant in larger cities, with prices projected to rise by 6.9% in Milan, 6.5% in Venice and 6% in Rome. The hotel market is also improving and seeing a growing presence of international chains.

Commercial real estate

According to Virginie Wallut, Director of Real Estate Research and Sustainable Investment at La Française Real Estate Managers, the European commercial real estate market showed signs of recovery in the first half of 2024, with year-on-year investment volumes increasing. This recovery emerged amid expectations that the European Central Bank (ECB) would begin to ease its monetary policy. Excluding France, European commercial real estate investment volumes rose by 11% year-on-year during the first half of 2024.

All asset classes experienced growth in investment volumes, with tourism leading the way (+62%), followed by logistics (+7%), healthcare (+4%) and both office and retail seeing modest gains of 1% each. However, core assets and diversification sectors (such as logistics, healthcare, tourism and managed housing) continue to be the most sought-after by investors.

Offices

According to BNP Paribas, European office investment volumes reached €18 billion in the first half of 2024, 11% down on the same period in 2023. However, the rate of decline has slowed significantly and some markets are experiencing growth, including Italy (+99%), Spain (+46%) Norway (+190%) and Poland (+190%). Office sector investment volumes are continuing to decline in key markets such as Germany (-31%), the UK (-26%) and France (-55%).

In central Paris, the overall office vacancy rate rose to 10% in 2023, yet prime rents increased by 7%, reaching a new record high of €1,067 per square metre. Similar trends can be observed in other key markets such as London, Amsterdam, Madrid and Berlin. In Italy, Milan continues to be the dominant market, followed by Rome, where demand for office space has been growing. According to Urti Re Projects, prime yields have risen to 4.5% in Milan and 4.75% in Rome.

Logistics

According to Abrdn Investment, the European logistics market has begun to stabilise. European logistics take-up reached 8.1 million square metres in the fourth quarter of 2023, higher than the long-term average. The conflicts in the Middle East highlighted the potential benefits of nearshoring and the importance of risk diversification in logistics operations. While logistics rents rose by 6.9% in 2023 compared to 9% in 2022, rental growth is expected to remain higher than the long-term average and to outstrip inflation rates through 2024 and 2025, as supply in prime locations remains constrained.

Retail

The retail sector has been impacted by the economic cycle. However, according to Retail Abrdn, the recent decline in inflation has caused real wage growth to turn sharply positive, bolstering consumer spending. Retail vacancy rates in Europe have fallen to an average of 3.8%, with the UK seeing even lower rates of 2%. Despite this, shopping centres continue to face structural challenges, with vacancy rates rising to 12.7% in the fourth quarter of 2023. These figures suggest that while investors need to remain cautious about income risks in the sector, retail warehouses present selective opportunities worth considering.