Market Economics

The changing face of the European real estate market

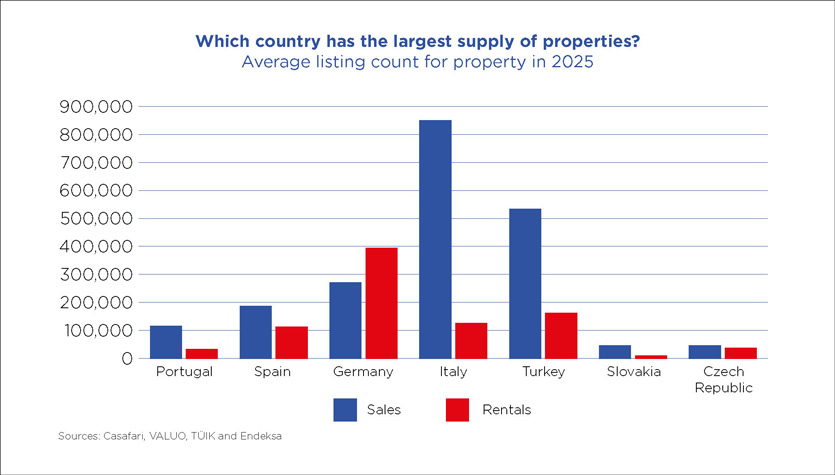

(May 2026) – Italy stands apart from other major European real estate markets in terms of its high inventory levels and strong appeal for foreign investors, who accounted for one in every five residential sales. According to the 2025 Housing Insider – European Real Estate Insights report by RE/MAX Europe, Italy recorded approximately 850,000 listings in 2025 – equivalent to 14 properties per 1,000 inhabitants. This stands in stark contrast to Germany, where supply shortages have restricted the market to just 3 properties per 1,000 residents.

This high housing availability gives the Italian market greater stability, allowing buyers to navigate a less competitive landscape than elsewhere in Europe while prioritising quality and energy efficiency. “Buyers in Italy are expressing new housing requirements, leading to a surge in demand for high-quality properties, particularly renovated, energy-efficient homes,” comments Dario Castiglia, CEO and Founder of RE/MAX Italia.

While Italy recorded relatively moderate overall price growth of +2.7% (+3.4% for apartments), other European markets faced significantly higher pressure due to supply scarcities and a lack of new-build projects. In Portugal, for example, average prices jumped by 17%, with apartments up by 20%, while Spain recorded 10% growth (apartments +15%). In Germany, the recovery was more modest at just 4%, while Turkey recorded a 9% decline, hit hard by exceptionally high interest rates.

This relative stability of the Italian market has generated strong international interest in the country’s property assets. One home in five was purchased by a foreign buyer in 2025, nearly double the 11% share recorded in 2024. Italy is now rivalling Spain as a top destination for high-net-worth investment. This market stability, coupled with a competitive tax regime, is attracting investors not only to large cities such as Rome and Milan but increasingly also towards prestigious tourist destinations.

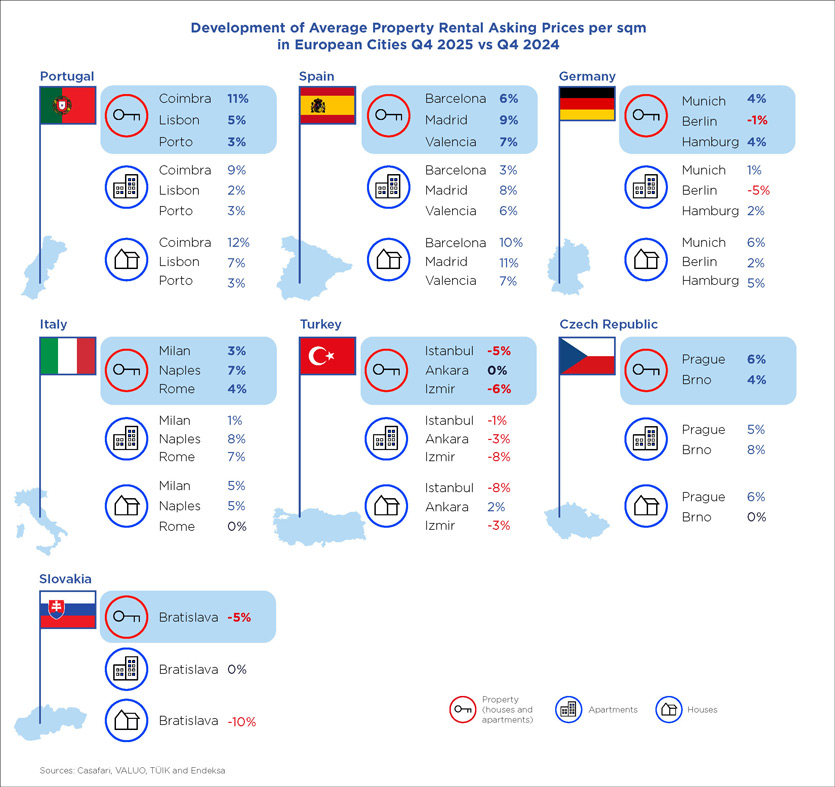

However, while Italy’s sales market is enjoying a period of comparative stability, the same cannot be said for rentals. According to data analysed in the RE/MAX report, rents rose significantly in 2025, with Spain (+9%) and Italy (+7%) topping the ranking for rental increases, followed by Portugal (+6%) and Germany (+2%). The more subdued growth in Germany is primarily due to regulatory caps and a market that has already reached its affordability limits.

The strong rental growth in 2025 was closely linked to baseline rent levels and the regulatory environment. In markets where rents were already high, affordability thresholds and regulatory constraints limited further acceleration. Germany offers the clearest example of this moderation. National rents grew by just 2% (€11 per sqm), with Munich up 4% (€23 per sqm) and Hamburg also rising by 4% (€18 per sqm), while Berlin saw a 1% decline (€19 per sqm). There was a significant disparity between property types. At a national level, apartment rents rose by 5% while single-family homes remained stable. In Munich, house rents increased by 6% compared to just 1% for apartments; conversely, in Berlin apartment rents fell by 5% while house rents grew by 2%. These modest fluctuations reflect high baseline prices coupled with regulatory cooling in major urban hubs, a trend further reinforced by the German government’s rent cap, which limits further increases.

Portugal, by contrast, recorded national rent growth of 6% (€12 per sqm), with dynamics varying by property type. At a national level, houses outperformed apartments (7% compared to 5%), a trend that was most evident in Lisbon where single-family homes rose by 7% while apartments increased by only 2%. Lisbon saw overall growth of 5% (€20 per sqm), while rental prices in Porto rose by 3% (€15 per sqm). The persistent volume of short-term lets in certain neighbourhoods has further squeezed the supply of long-term housing.

Italy has seen a similar plateau effect in its most expensive city. While rents climbed by 7% at a national level to €11 per sqm, they rose by just 3% in Milan to €17 per sqm (compared to 4% in Rome to €14 per sqm). Although apartment rents increased by 8% nationally compared to 5% for houses, Milan’s more subdued growth suggests that the country’s most expensive rental market is hitting an affordability ceiling, a trend less evident in lower-priced cities such as Naples (+7%, €10 per sqm).