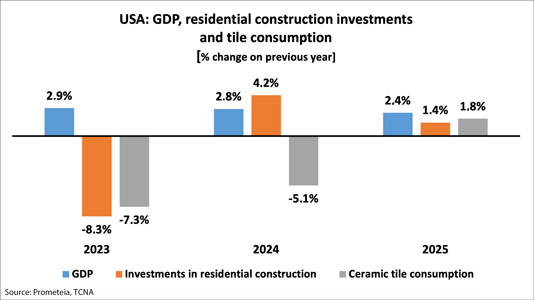

(April 2025) | Following solid economic growth of approximately 2.8% in 2024, the US economy is expected to continue expanding in 2025. This trajectory will be supported by a dynamic labour market and steady wage growth – albeit at a slower pace than in recent years – leading to a projected GDP increase of around 2.4%. At the same time, early signs of a slowdown are beginning to surface, including a persistently low savings rate and weakening consumer confidence. Despite this, the ongoing housing shortage, together with a potential decline in interest rates, is likely to support residential investment, which is forecast to grow by around 1.4% in 2025 following a 4.2% rebound in 2024.

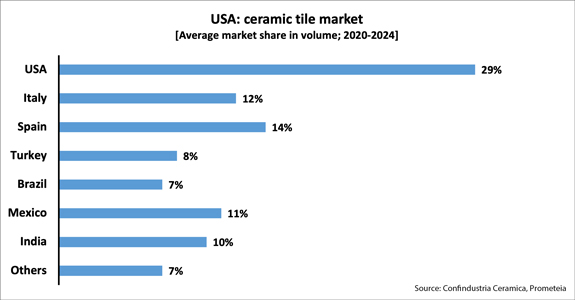

The US ceramic tile market is the world’s largest importer, accounting for more than 6% of global imports by volume and 8% by value. Between 2020 and 2024, domestic producers maintained an average market share of around 29%, while imports accounted for approximately 70% of total ceramic tile consumption, which averaged around 270 million square metres annually. The market is also characterised by a highly diversified supplier base. European producers, particularly Italy and Spain, together hold about a quarter of the market, while Latin American countries such as Mexico and Brazil account for about 18% of total US consumption. Among Asian suppliers, India has rapidly expanded its exports in recent years, gaining significant market share alongside other Southeast Asian countries. Between 2019 and 2023, US imports from India grew by more than 31 million square metres, establishing it as the top supplier by volume in the space of just a few years.

According to figures provided by the Tile Council of North America, US ceramic tile consumption reached 250.9 million square metres in 2024, down 5.1% compared to 2023. Domestic sales fell by around 9%, while total imports dropped by 3.5%. Italian producers, however, saw a recovery in sales to the US compared to 2023 in contrast to all other major exporters, whose sales continued to decline.

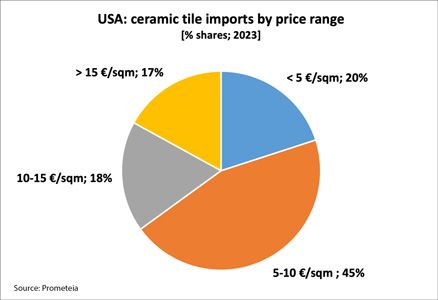

In the import market, however, tariffs continue to represent a significant concern. The possible introduction of a flat-rate tariff applied uniformly to all foreign suppliers would disproportionately affect exporters operating in higher-priced segments, where the impact would be most pronounced.

Si informa che questo sito utilizza cookie, anche di terze parti, al fine di analizzare il traffico sul sito e personalizzare i contenuti e gli annunci più adatti a te.

Cookie Policy{kind=link}

{kind=link}

{kind=link}